Most investors know Ajinomoto for MSG and seasonings.

Few realize it also sits at the heart of advanced semiconductor packaging.

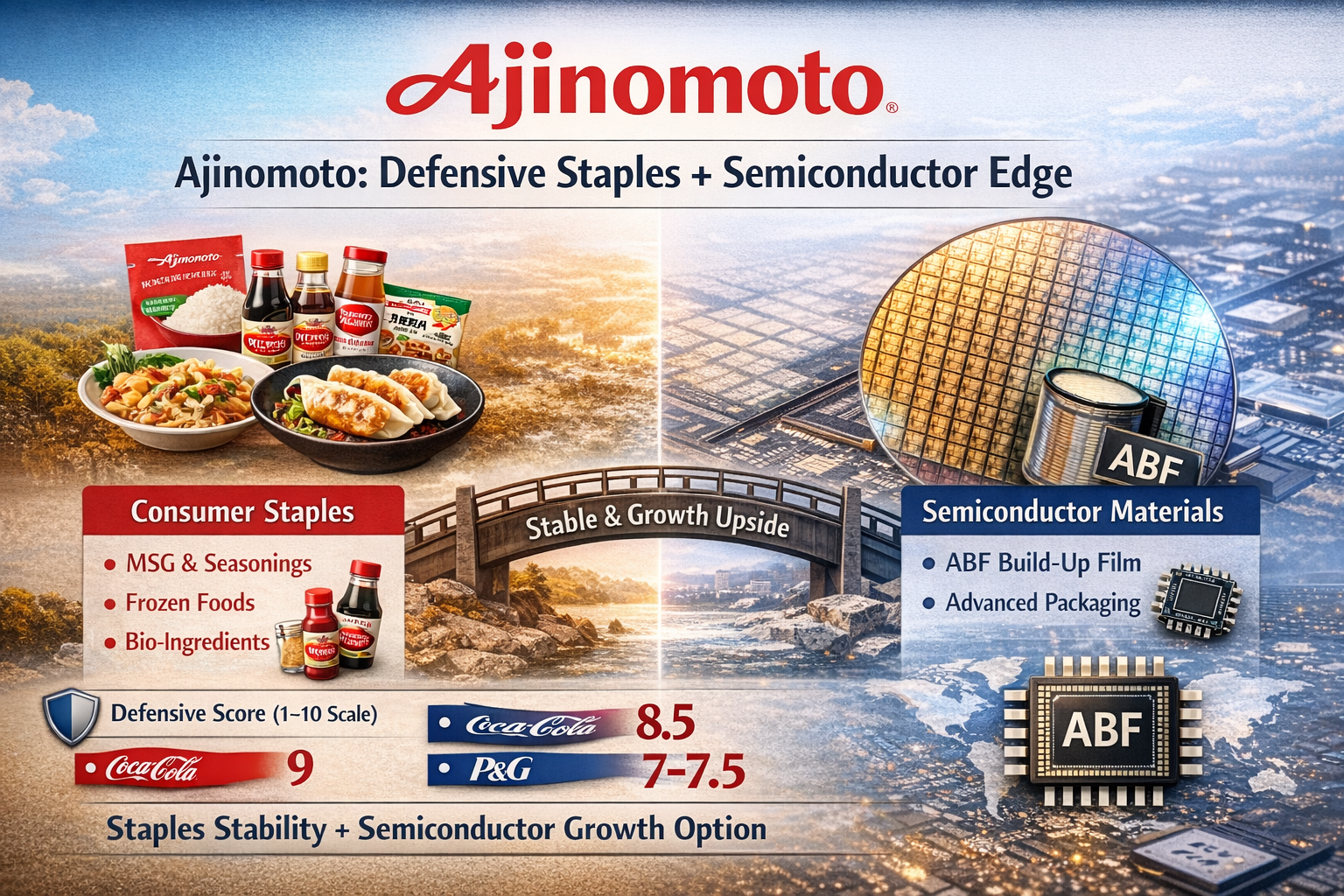

Ajinomoto is a Japanese global company built around:

- Food & Seasonings

- Amino Acid / Bioscience Technologies

- Electronic Materials — most notably Ajinomoto Build-up Film (ABF)

This mix creates a unique profile:

consumer-staples stability + semiconductor exposure.

What Ajinomoto Does

1️⃣ Seasonings & Foods — The Core Cash Engine

- MSG / umami seasonings

- Flavor seasonings and sauces

- Consumer packaged foods

- Strong presence in Japan and across Asia

This segment provides steady, recurring demand. These are everyday essentials, not discretionary luxuries.

2️⃣ Frozen Foods

- Domestic and overseas frozen food portfolio

- More cyclical and margin-sensitive

- Adds scale and distribution strength

3️⃣ Healthcare & Others — Where ABF Lives

This segment includes:

- Functional materials (electronic materials, including ABF)

- Bio-pharma services and ingredients

- Amino acids for pharma and food applications

This is the segment that transforms Ajinomoto from a traditional food company into a strategic materials player.

Understanding ABF (Ajinomoto Build-up Film)

ABF is a high-performance insulating film used in advanced semiconductor substrates. It enables:

- High layer counts

- Fine circuit patterning

- Strong electrical and thermal performance

It is essential for:

- CPUs

- GPUs

- AI accelerators

- High-performance servers

Without ABF-type materials, modern advanced packaging would not function at current performance levels.

Is Ajinomoto the Only Producer?

Short answer:

Not literally the only producer — but overwhelmingly dominant.

Ajinomoto (through its affiliate Ajinomoto Fine-Techno) is estimated to hold roughly 95–98% global market share in ABF film production.

That level of dominance is rare in semiconductor materials.

Some smaller alternative suppliers occasionally cited include:

- Sekisui Chemical Co., Ltd.

- WaferChem

- Taiyo Ink

However, none approach Ajinomoto’s scale or capabilities in high-density applications.

Important Distinction: ABF Film vs ABF Substrate

Many companies manufacture ABF substrates, but most rely on Ajinomoto’s film.

Major substrate makers include:

- Unimicron Technology Corp.

- Ibiden Co., Ltd.

- Nan Ya PCB Corporation

- Shinko Electric Industries Co., Ltd.

- AT&S

Ajinomoto supplies the material layer — it does not compete in substrate board manufacturing.

Business Mix: How Large Is the ABF Segment?

Ajinomoto does not break out ABF revenue separately. It sits inside:

Healthcare & Others → Functional Materials

For fiscal year ended March 31, 2025:

- Total sales: ¥1,530.5B

- Healthcare & Others sales: ¥328.3B (~21% of total)

- Total business profit: ¥159.3B

- Healthcare & Others business profit: ¥38.1B

ABF is a slice of this ~21% revenue bucket, which tends to carry higher margins than typical food operations.

Moat Analysis

Strongest Moat Area: ABF / Electronic Materials

- High customer qualification barriers

- Deep materials science know-how

- Long switching cycles

- Embedded in AI and HPC supply chains

- Extremely limited credible competition

At the business-unit level, ABF displays narrow-to-wide moat characteristics.

Moderate Moat Area: Food & Seasonings

- Strong brands and distribution

- Recurring demand

- Exposed to commodity input costs

Durable — but not a structural toll booth like Visa or ASML.

Ajinomoto as a Defensive Position

Ajinomoto functions best as a defensive-growth hybrid.

The food and seasoning businesses provide stable demand and smooth earnings during downturns. The amino acid and bio-ingredient businesses add structural healthcare exposure.

Meanwhile, ABF introduces semiconductor and AI-linked upside.

The result:

- Defensive consumer staples foundation

- Structural healthcare exposure

- Select semiconductor growth optionality

Compared to pure semiconductor equipment companies like Applied Materials, Inc. or Lam Research Corporation, Ajinomoto typically experiences lower volatility because its food business cushions industry cycles.

Defensive Score (Relative)

On a 1–10 defensive scale:

- Coca-Cola Company: 9

- Procter & Gamble: 8.5

- Ajinomoto Co., Inc.: 7–7.5

This places Ajinomoto below pure consumer staple giants, but meaningfully more defensive than most semiconductor equipment names.

Financial Snapshot

Fiscal Year Ended March 31, 2025:

- Sales: ¥1,530.5B

- Business profit: ¥159.3B

Fiscal Year Ended March 31, 2024:

- Sales: ¥1,439.2B

- Business profit: ¥147.6B

- Operating profit: ¥146.6B

- Net profit attributable to owners: ¥87.1B

Growth has been steady, supported by both staples stability and materials expansion.

Key Risks

- Semiconductor cycle volatility

- Food commodity inflation and FX exposure

- Potential long-term competition in ABF (though currently limited)

U.S. Trading Information

Ajinomoto trades primarily in Japan under:

- 2802.T (Tokyo Stock Exchange)

In the U.S., it is available via ADR:

- AJINY (OTC market)

The ADR is not listed on NYSE or Nasdaq and trades with lower liquidity compared to major exchange-listed ADRs.

Bottom Line

Ajinomoto is not a pure semiconductor powerhouse like ASML Holding N.V..

It is better described as:

Stable consumer staples cash flow + a strategically valuable semiconductor materials franchise.

For investors seeking resilience with moderate growth exposure and geographic diversification, Ajinomoto occupies a unique middle ground between traditional consumer staples and semiconductor cyclicals.